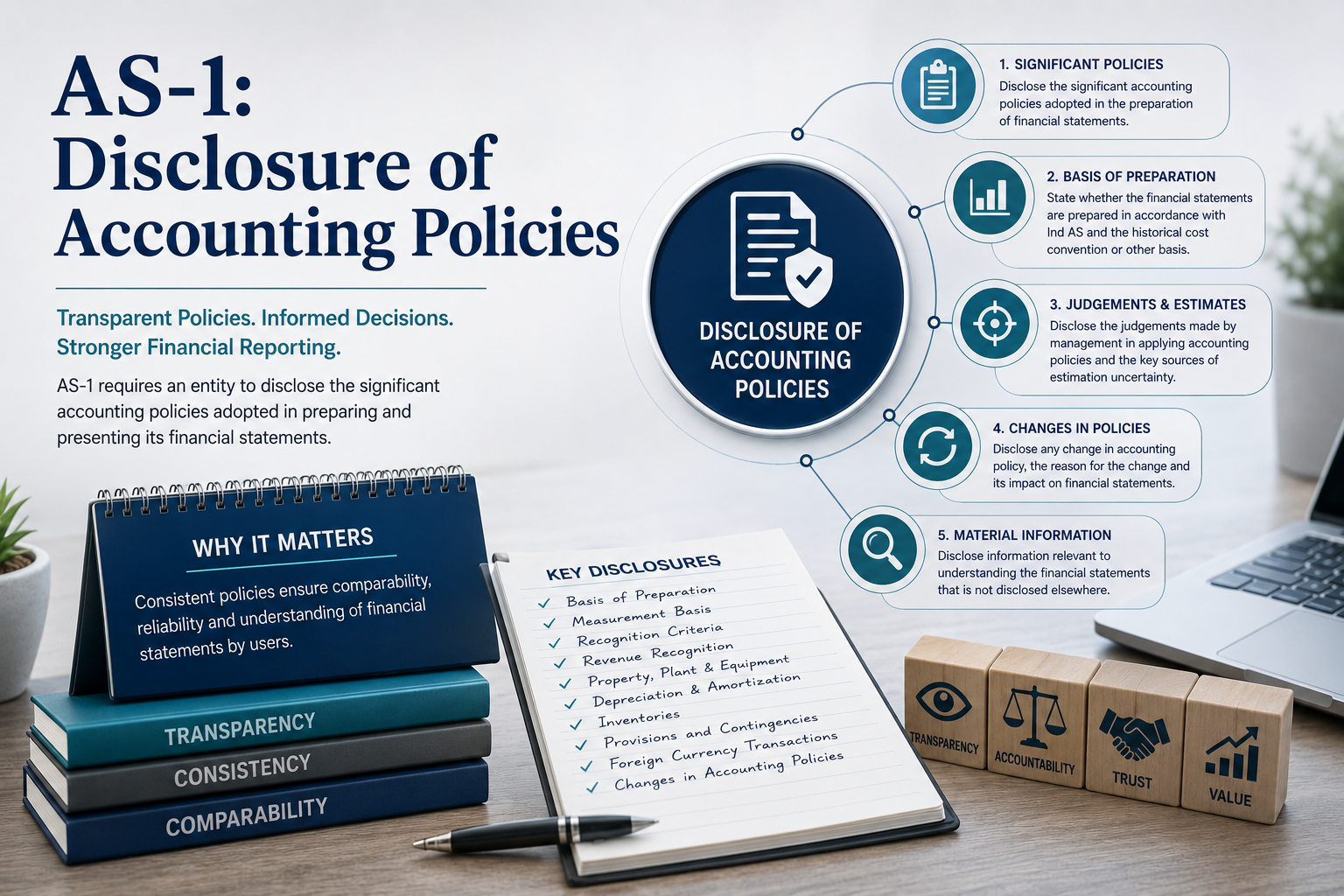

Accounting Standard 1 (AS-1) is the bedrock of the financial reporting framework in India. It mandates that all significant accounting policies adopted in the preparation and presentation of financial statements should be disclosed in one place. The primary objective is to ensure that the users of financial statements can understand and compare the financial health of an entity accurately.

1. Fundamental Accounting Assumptions (FAA)

There are three fundamental assumptions that are "assumed" to be followed in every set of financial statements. AS-1 states that if these are followed, no specific disclosure is required. However, if any of these are NOT followed, that fact must be explicitly disclosed.

Going Concern

The entity will continue its operations for the foreseeable future and has neither the intention nor the necessity of liquidation.

Consistency

It is assumed that accounting policies are consistent from one period to another to allow meaningful comparison.

Accrual

Revenues and costs are recognized as they are earned or incurred, not as money is received or paid.

2. Considerations in the Selection of Accounting Policies

While there are many ways to record a transaction, AS-1 prescribes three major considerations that management must use when selecting a policy:

- Prudence: In view of the uncertainty, profits should not be anticipated, but all recognized losses should be provided for. (Example: Provision for Bad Debts)

- Substance Over Form: Transactions should be accounted for in accordance with their economic reality and not merely their legal form. (Example: Hire Purchase Assets)

- Materiality: Financial statements should disclose all items that are "material"—meaning items that could influence the economic decisions of the users.

3. Common Areas Requiring Disclosure

Entities often have different policies for the same area. You must disclose which one you use for:

| Accounting Area | Example of Policies |

|---|---|

| Valuation of Inventories | FIFO, Weighted Average, etc. |

| Depreciation | Straight Line Method (SLM) or WDV Method. |

| Revenue Recognition | Point of Sale vs. Percentage of Completion. |

| Foreign Currency Items | Conversion rates used for monetary/non-monetary items. |

4. Change in Accounting Policies

A change in accounting policy should only be made if:

- It is required by Statute (Law).

- It is required for compliance with an Accounting Standard.

- It results in a better presentation of financial statements.

Disclosure of Change:

If a change has a material effect, the entity must disclose:

• The nature of the change.

• The financial impact (the amount by which items in the financial statements are affected).

Practical Tip for Practitioners

All significant accounting policies should be disclosed as "Schedule 1" or "Note 1" to the financial statements. This is not just a procedural requirement but a legal safeguard. Ensure that the "Notes to Accounts" are not scattered; AS-1 specifically requires a single location for these disclosures to ensure they are not missed by the auditor or stakeholders.