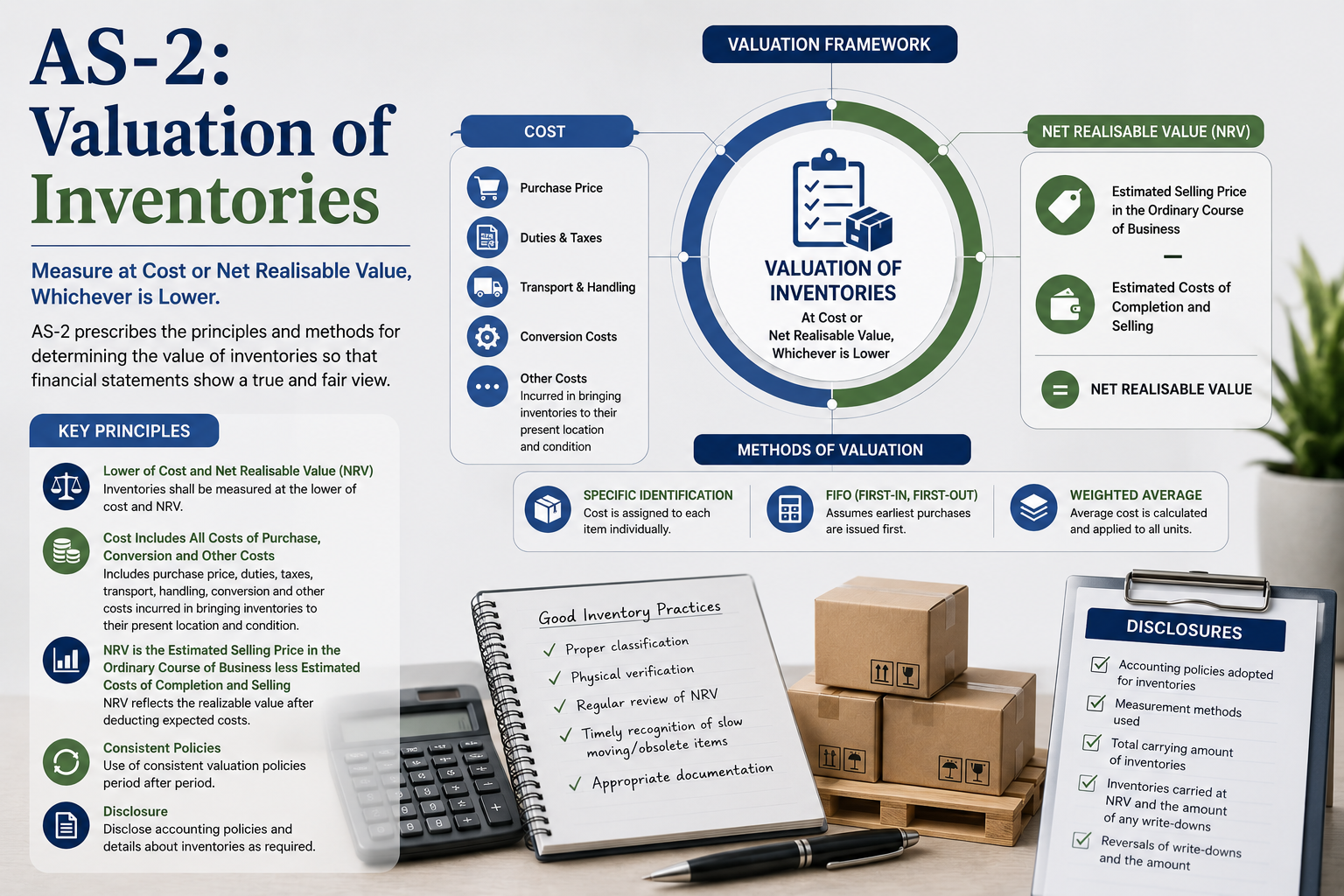

1. Core Measurement Principle

Inventories should be valued at the LOWER of:

COST or NET REALIZABLE VALUE (NRV)

2. Components of Cost

The cost of inventories should comprise all costs of purchase, costs of conversion, and other costs incurred in bringing the inventories to their present location and condition.

Costs of Purchase

- Purchase price

- Duties and taxes (non-refundable)

- Freight Inwards

- Less: Trade discounts/rebates

Costs of Conversion

- Direct Labour

- Fixed Production Overheads (allocated on normal capacity)

- Variable Production Overheads

3. Exclusions from Cost

These costs must be recognized as expenses in the period they occur:

- Abnormal amounts of wasted materials, labour, or other costs.

- Storage costs (unless necessary in the production process).

- Administrative overheads that do not contribute to bringing inventories to their present location.

- Selling and distribution costs.

4. Cost Formulas

For items that are ordinarily interchangeable, AS-2 permits:

- FIFO (First-In, First-Out): Assumes items purchased first are sold first.

- Weighted Average Cost: Cost is determined from the weighted average of the cost of similar items at the beginning of a period and during the period.

Note: LIFO (Last-In, First-Out) is strictly prohibited under AS-2.